Your Business Credit Score Guide

Learn more about the key areas that determine your score, how to read your business credit report and, above all, how you can improve it over time.

Learn more about the key areas that determine your score, how to read your business credit report and, above all, how you can improve it over time.

Your business credit score works very much like your personal one. Banks and lenders in general use it to make informed decisions about the risk your business presents when you apply for a loan or a financial product. In short, your business credit score may affect whether your application will be accepted and impact the rates you will be offered.

So understanding what it is, why it is important and how you can improve it is a big step in your entrepreneurial journey. We will explain some of the key areas that determine your score, how to read your business credit report and, above all, how you can improve it over time.

The Credit Passport® business credit score provides a clear picture of your business. It includes:

Credit Passport is the first real-time credit score designed to bridge the gap between the financial industry and business owners. Powered by Open Banking, it provides an instant, powerful and clear view of a company credit quality.

Credit Passport uses your bank data to show you how the financial system sees you in real time. By having a full overview of your financial reputation, you can improve your score and take confident and deliberate steps to grow build financial strength and grow your business.

The Credit Passport has two elements:

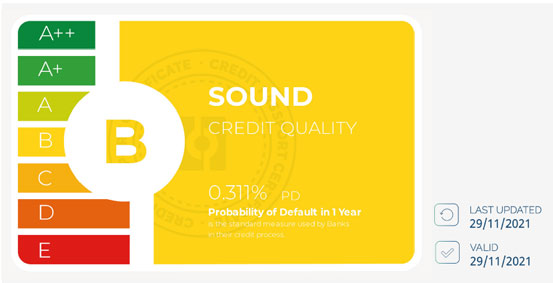

Credit Passport is special, as it is constructed to reflect the internal rating systems of large bank, and this PD scale is in line with banking principles set out in international banking regulations. It is the chance (as a percentage) that your business will be unable to meet its payment obligations within 90 days of their due date in the coming 12 months from the date of the score. This is a complicated concept, but it is very useful for lenders to see, as it means they can accurately price loans with the confidence that they will be covered, and they do not have to increase the rates to ‘price the unknown’.

For example, a company with a 0.5% PD will be scored as a B, which is all you really need to know. For the lender, it means that for a 1 year loan, there is a 0.5% chance it that payments will be missed. In other words, if they lent to 200 companies with this score, one of them would default. However, if the loan term was 5 years, out of 200 companies, then 5 of them would default before the loan was paid back. This way, they know what interest rate they can charge and not be overall at a loss.

In our scale, most small companies in the UK will score as a C or B, which we also refer to as Moderate or Sound Credit Quality. Anyone with a B or above is doing really well, and is able to communicate this with a Credit Passport web badge, to boost customer and supplier confidence.

A higher credit score, which reflects a good company’s performance and creditworthiness, indicates low risk to potential lenders, suppliers and customers. On the contrary, a lower credit score (LOW & CRITICAL as per our scale) may mean that you may have difficulty accessing credit and financial products, or end up paying more for finance.

Your business credit score is calculated based on a variety of inputs. On your financial history, and your track-record of paying back previous business loans and borrowings, as well as how timely you were with the payments and in Credit Passport’s case, also your cashflow management and your current exposure to the financial system as indicated via your connected bank accounts.

Key aspects that might affect your financial assessment are:

Most credit scores are created by looking at the amount of debt you or your company has with the financial system. For companies, it is also common to look at your most recent filed company accounts. However, these accounts usually reflect finances from 12 or 18 months earlier, and the debt only tells one side of the story.

Credit Passport is different. It is the only credit score for business created in real-time, that reflects the fast-changing nature of SMEs.

Credit Passport connects to your bank accounts using Open Banking and updates daily. It has been designed from the ground up to reflect how your own bank views and makes lending decisions about you, giving you rare insight into what you need to do to be seen in the best light, how to be more financially resilient, and how to access the lowest lending rates.

Remember that a good business credit score is about more than just not defaulting on your loans. It also means you are a resilient and financially healthy company that is well placed for financial growth or to survive unexpected challenges. Keeping a good Credit Passport score means your business is strong, healthy and ready.

Constantly monitoring your credit score will help you make informed and confident financial decisions. It is very important to be aware of your financial status and immediately take action if anything is impacting it negatively to avoid a performance dip.

Focus on the next step with Credit Passport Plus Plan for just £20 per month to access your full real-time digital report, including the specific indicators that are having a positive or negative effect on your business credit score, analyse your company’s spending impact and boost your brand credibility.